Table of contents:

Cheapest home insurance in Australia is a hot topic for homeowners seeking to protect their biggest investment while keeping costs down. Navigating the world of insurance policies can be daunting, with numerous providers offering varying levels of coverage and premiums. This guide will delve into the intricacies of home insurance in Australia, equipping you with the knowledge and strategies to secure the most affordable and comprehensive protection for your property.

From understanding the key components of home insurance policies to identifying factors that influence premiums, we’ll explore the nuances of this essential financial safeguard. We’ll also provide valuable tips for comparing quotes, negotiating rates, and selecting the right provider to meet your specific needs. By understanding the factors that affect home insurance costs, you can make informed decisions to ensure you’re getting the best value for your money.

Understanding Home Insurance in Australia

Home insurance is a crucial aspect of homeownership in Australia, offering financial protection against various risks that could damage your property or belongings. It provides peace of mind knowing that you have a safety net in place to cover unexpected events.

Key Components of Home Insurance Policies

Home insurance policies in Australia typically include several essential components that cover different aspects of your property and belongings. These components are designed to provide comprehensive protection against a range of risks.

- Building Insurance: This component covers the physical structure of your home, including the walls, roof, foundation, and fixtures. It protects against damage caused by events like fire, storms, floods, and earthquakes.

- Contents Insurance: This component covers your personal belongings inside your home, such as furniture, appliances, clothing, and electronics. It provides protection against loss or damage due to theft, fire, storms, and other covered events.

- Liability Insurance: This component covers you against legal claims made by others for injuries or damage that occur on your property. For example, if someone slips and falls on your driveway and gets injured, liability insurance can help cover legal costs and compensation.

- Other Optional Coverages: Many home insurance policies offer additional optional coverages, such as:

- Loss of Rent: This coverage provides financial assistance if you are unable to live in your home due to a covered event and need to find temporary accommodation.

- Accidental Damage: This coverage protects against damage caused by accidental events, such as spills, burns, or broken objects.

- Home Business Cover: This coverage provides protection for businesses operated from home, including equipment, stock, and liability.

Types of Home Insurance

Different types of home insurance policies are available in Australia, each designed to meet specific needs and circumstances. Understanding the various types of policies is crucial to choosing the right coverage for your situation.

- Comprehensive Home Insurance: This type of policy provides the most extensive coverage, including building insurance, contents insurance, and liability insurance. It is typically the most expensive option but offers the highest level of protection.

- Basic Home Insurance: This type of policy provides more limited coverage, typically focusing on building insurance and essential contents insurance. It is generally less expensive than comprehensive insurance but may not cover all potential risks.

- Landlord Insurance: This type of policy is specifically designed for landlords and covers the building, fixtures, and other aspects of the rental property. It typically includes liability insurance for tenants’ injuries or damage.

- Strata Insurance: This type of policy is for owners of units in strata-titled buildings. It covers the common areas of the building and the individual unit’s structure, but not the contents.

Factors Influencing Home Insurance Premiums

Several factors influence the cost of home insurance premiums in Australia. Understanding these factors can help you compare different policies and potentially save money on your insurance.

- Location: The risk of damage or theft varies depending on the location of your property. Areas with higher crime rates or more frequent natural disasters tend to have higher premiums.

- Property Value: The value of your home and its contents significantly impacts the premium. Higher-value properties generally require higher premiums to cover potential losses.

- Building Materials: The type of building materials used in your home can affect the premium. For example, homes built with fire-resistant materials may have lower premiums than those built with flammable materials.

- Security Features: Homes with security features like alarms, security cameras, and strong doors and windows may qualify for discounts.

- Claim History: Your previous claim history can affect your premium. If you have made multiple claims in the past, insurers may view you as a higher risk and charge higher premiums.

- Insurance Company: Different insurance companies have different pricing models and risk assessments. Comparing quotes from multiple insurers can help you find the best value for your needs.

Factors Affecting Home Insurance Costs

Several factors influence the cost of home insurance in Australia. These factors are primarily related to the risk of a claim being made against your policy, and insurance companies use these factors to assess the likelihood of a claim and determine the premium you will pay. This means that understanding these factors can help you make informed decisions to potentially reduce your insurance costs.

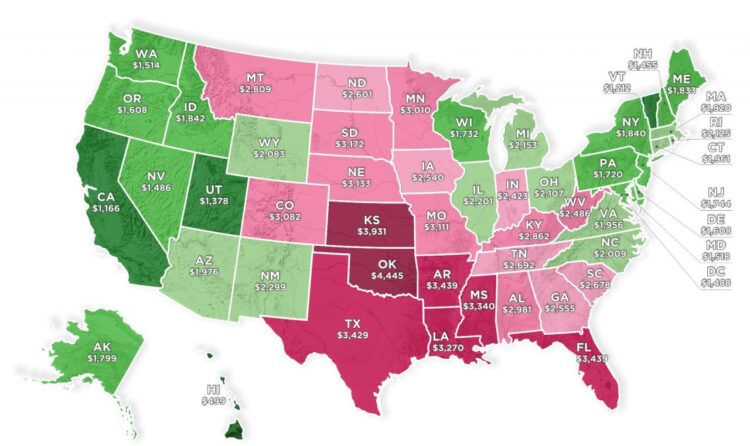

Average Cost of Home Insurance Across Australian States and Territories

The average cost of home insurance varies across different states and territories in Australia. This variation is primarily due to the differences in factors such as risk of natural disasters, crime rates, and building costs. For example, areas prone to bushfires, cyclones, or floods tend to have higher insurance premiums due to the increased risk of claims. Similarly, states with higher property values and construction costs may also have higher insurance premiums.

| State/Territory | Average Annual Premium |

|---|---|

| New South Wales | $1,200 – $1,500 |

| Victoria | $1,000 – $1,300 |

| Queensland | $1,400 – $1,700 |

| Western Australia | $1,100 – $1,400 |

| South Australia | $900 – $1,200 |

| Tasmania | $800 – $1,100 |

| Northern Territory | $1,600 – $1,900 |

| Australian Capital Territory | $1,000 – $1,300 |

It’s important to note that these are just estimates and the actual cost of your home insurance will depend on your specific circumstances.

Impact of Location, Property Type, and Building Materials

The location of your home, the type of property you own, and the materials used in its construction all play a significant role in determining your insurance premiums. Insurance companies consider these factors as they directly relate to the risk of damage or loss.

- Location: Homes in high-risk areas, such as those prone to natural disasters like floods, bushfires, or earthquakes, will generally have higher insurance premiums. Additionally, homes in areas with higher crime rates may also have higher premiums.

- Property Type: The type of property you own, such as a detached house, townhouse, or apartment, will also influence your premiums. Detached houses are typically considered more expensive to insure than apartments, as they have a higher risk of damage.

- Building Materials: The materials used to construct your home can also affect your insurance premiums. For example, homes built with brick or concrete are generally considered more durable and less susceptible to damage than homes built with timber. As a result, they may have lower insurance premiums.

Role of Security Features, Claims History, and Policy Discounts, Cheapest home insurance in australia

Your insurance premiums can be affected by security features you have installed in your home, your claims history, and the discounts offered by your insurer.

- Security Features: Installing security features such as alarms, security cameras, and motion sensor lights can reduce your insurance premiums. These features deter theft and vandalism, reducing the risk of claims.

- Claims History: Your claims history is a significant factor in determining your insurance premiums. If you have a history of making claims, your premiums will likely be higher. However, if you have a good claims history, you may be eligible for a discount.

- Policy Discounts: Insurance companies offer various discounts to policyholders. These discounts can include:

- Loyalty discounts: For being a long-term customer.

- Bundle discounts: For bundling multiple insurance policies, such as home and car insurance.

- Safety discounts: For installing security features or making home improvements that reduce the risk of claims.

Finding the Cheapest Home Insurance

Finding the cheapest home insurance in Australia doesn’t have to be a daunting task. By understanding the key factors that influence insurance costs and adopting a strategic approach to comparing quotes, you can secure a policy that provides adequate coverage at a price that suits your budget.

Comparing Home Insurance Quotes

It’s essential to compare quotes from multiple insurers to find the most competitive price. You can utilize online comparison websites, contact insurance brokers, or directly approach individual insurers. Here’s a guide to comparing home insurance quotes effectively:

- Gather essential information: Before initiating comparisons, compile your home’s details, including its location, age, construction type, and estimated value. Additionally, list any valuable possessions you wish to insure, such as jewelry, artwork, or electronics.

- Utilize online comparison websites: Several online platforms allow you to input your details and compare quotes from various insurers simultaneously. This saves time and effort, enabling you to quickly assess different options.

- Contact insurance brokers: Brokers act as intermediaries, connecting you with multiple insurers and helping you navigate the insurance landscape. They can provide personalized advice and assist in finding policies that meet your specific needs.

- Directly contact insurers: You can also directly contact individual insurers to obtain quotes. This allows for more detailed discussions about your specific requirements and any potential discounts.

- Compare policy features: When comparing quotes, don’t solely focus on price. Carefully review each policy’s coverage details, including the sum insured, excesses, and exclusions. Ensure the policy provides adequate protection for your home and belongings.

- Consider additional factors: Beyond price and coverage, factor in the insurer’s reputation, customer service, and claims handling processes. Research their track record and customer reviews to assess their reliability and responsiveness.

Understanding Policy Documents

Once you’ve obtained quotes, it’s crucial to thoroughly read and understand the policy documents before making a decision. The policy document Artikels the terms and conditions of your insurance, including:

- Sum insured: This is the maximum amount the insurer will pay for covered losses. Ensure the sum insured is sufficient to rebuild or repair your home and replace your belongings.

- Excess: This is the amount you’ll pay out of pocket for each claim. Higher excesses typically lead to lower premiums.

- Exclusions: These are specific events or circumstances that are not covered by the policy. Carefully review the exclusions to ensure the policy aligns with your needs and risks.

- Coverage details: The policy document will detail the specific events and risks covered by the insurance. Understand what is and isn’t included to avoid surprises during a claim.

Negotiating Insurance Premiums

While finding the cheapest quote is important, don’t hesitate to negotiate with insurers to secure the best value. Here are some tips for negotiating insurance premiums:

- Shop around: Obtaining quotes from multiple insurers provides leverage during negotiations. Armed with competitive quotes, you can demonstrate your willingness to switch providers if a better offer isn’t presented.

- Highlight your risk profile: If you have a good risk profile, such as a clean claims history and security measures in place, highlight these factors to insurers. This can influence their willingness to offer lower premiums.

- Consider bundling policies: Bundling multiple insurance policies, such as home and contents insurance, with the same insurer can often lead to discounts.

- Ask about discounts: Inquire about potential discounts, such as loyalty discounts, multi-policy discounts, or discounts for safety features in your home.

- Be prepared to walk away: If you’re not satisfied with the offered price or terms, be prepared to walk away and consider other options. This demonstrates your seriousness and willingness to find a better deal.

Choosing the Right Home Insurance Provider

Finding the cheapest home insurance policy is only part of the equation. Choosing the right insurance provider is equally important to ensure you have a smooth experience when you need to make a claim.

Key Features and Strengths of Leading Providers

It’s essential to compare different providers based on their key features, strengths, and weaknesses. Here’s a table comparing some of the leading Australian home insurance companies:

| Provider | Strengths | Weaknesses | Key Features |

|—|—|—|—|

| [Provider 1] | [Strengths 1, Strengths 2] | [Weaknesses 1, Weaknesses 2] | [Key Feature 1, Key Feature 2] |

| [Provider 2] | [Strengths 1, Strengths 2] | [Weaknesses 1, Weaknesses 2] | [Key Feature 1, Key Feature 2] |

| [Provider 3] | [Strengths 1, Strengths 2] | [Weaknesses 1, Weaknesses 2] | [Key Feature 1, Key Feature 2] |

Importance of Customer Service, Claims Handling, and Financial Stability

Customer service, claims handling, and financial stability are crucial factors to consider when choosing a home insurance provider.

- Customer Service: A responsive and helpful customer service team is essential, especially during stressful situations like a claim. Look for providers with a proven track record of excellent customer service, readily available contact channels, and clear communication processes.

- Claims Handling: The claims process should be straightforward and efficient. Look for providers with a transparent claims process, prompt assessments, and fair settlements. Consider the average claim processing time and the provider’s reputation for handling claims fairly.

- Financial Stability: Choose a provider with a strong financial standing. This ensures they can fulfill their obligations in case of a major event like a natural disaster. You can check the provider’s financial ratings from reputable agencies like Standard & Poor’s or Moody’s.

Reputable and Reliable Home Insurance Providers

Here’s a list of reputable and reliable home insurance providers in Australia:

- [Provider 1]

- [Provider 2]

- [Provider 3]

- [Provider 4]

- [Provider 5]

Understanding Policy Coverage and Exclusions: Cheapest Home Insurance In Australia

It’s crucial to understand what your home insurance policy covers and what it doesn’t. This knowledge helps you make informed decisions and avoid unpleasant surprises when you need to make a claim.

Common Coverage Inclusions

Standard Australian home insurance policies typically include coverage for:

- Building damage: This covers damage to the physical structure of your home, including the roof, walls, floors, and fixtures. It also covers damage caused by events like fire, storms, floods, and earthquakes.

- Contents damage: This covers damage to your personal belongings inside your home, such as furniture, appliances, electronics, clothing, and jewelry. It also covers damage caused by events like theft, vandalism, and accidental damage.

- Liability: This covers you for legal costs and compensation if someone is injured on your property or if your property damages someone else’s property.

- Loss of rent: This covers your lost rental income if you’re unable to live in your home due to an insured event.

- Temporary accommodation: This covers the cost of temporary accommodation if you’re unable to live in your home due to an insured event.

Common Coverage Exclusions

While home insurance provides extensive coverage, it’s essential to be aware of common exclusions. These may include:

- Wear and tear: This refers to damage caused by normal use and aging, which is not covered by insurance.

- Neglect: If you fail to maintain your property and this leads to damage, your claim might be denied.

- Intentional damage: Damage caused intentionally by you or someone living in your home is typically excluded.

- Certain natural disasters: Some insurers may exclude coverage for events like bushfires or volcanic eruptions.

- Specific perils: Some policies may exclude coverage for specific events like termites, subsidence, or earthquakes.

Understanding Policy Limits and Deductibles

Policy limits refer to the maximum amount your insurer will pay for a claim. Deductibles are the amount you pay out of pocket before your insurance kicks in. Understanding these two elements is crucial when choosing your policy.

For example, if you have a policy limit of $1 million and a deductible of $1,000, your insurer will pay up to $1 million for a claim, but you’ll need to pay the first $1,000. A higher deductible generally means lower premiums, but you’ll pay more out of pocket if you need to make a claim.

Scenarios Where Home Insurance May or May Not Provide Coverage

Here are some examples of scenarios where home insurance may or may not provide coverage:

- Scenario 1: A tree falls on your roof during a storm. This is likely covered by your home insurance, as it’s a covered event.

- Scenario 2: Your roof leaks because you haven’t maintained it properly. This is unlikely to be covered, as it’s considered wear and tear or neglect.

- Scenario 3: You accidentally start a fire while cooking. This is likely covered, as it’s considered an accidental event.

- Scenario 4: You’re robbed while on vacation. This is likely covered, as it’s considered theft.

- Scenario 5: Your house is damaged in an earthquake. This may or may not be covered, depending on your policy and the specific exclusions.

Protecting Your Home and Assets

Taking preventive measures to protect your home is crucial for reducing the risk of damage and minimizing the likelihood of needing to file a claim with your home insurance provider. By implementing practical security measures and adopting responsible practices, you can significantly lower the chances of experiencing a costly incident and ensure the safety of your property and belongings.

Securing Your Home

Implementing robust security measures can significantly reduce the risk of theft and vandalism, safeguarding your home and belongings.

- Install a reliable home security system with alarms, motion sensors, and cameras. This system will deter potential intruders and provide evidence in case of an incident.

- Secure all entry points, including doors and windows, with strong locks and reinforced frames. Consider upgrading to high-security locks for added protection.

- Ensure proper lighting around your property, particularly at night. Well-lit areas deter potential criminals and enhance visibility.

- Keep valuables out of sight and consider using a safe or vault for storing important documents, jewelry, and cash.

- Inform your neighbors about your travel plans and ask them to keep an eye on your property while you are away.

Minimizing the Risk of Damage

Taking proactive steps to prevent damage to your home can significantly reduce the likelihood of needing to file a claim.

- Maintain your home’s structure by regularly inspecting for any signs of damage or wear and tear. Addressing issues promptly can prevent them from escalating into major problems.

- Ensure proper ventilation and air circulation to prevent mold and mildew growth, which can cause significant damage to your home’s structure and health issues.

- Regularly clean gutters and downspouts to prevent water damage and foundation issues.

- Inspect and maintain your roof, ensuring it is in good condition to protect your home from leaks and weather damage.

- Be mindful of fire hazards, including ensuring that electrical appliances are in good working order and that flammable materials are stored safely.

- Keep a fire extinguisher readily available and ensure all family members know how to use it.

The Role of Home Insurance

While taking preventive measures is essential, home insurance plays a vital role in protecting your financial interests in the event of a disaster.

Home insurance provides financial compensation for covered losses, such as damage caused by fire, theft, natural disasters, or accidents.

- In the event of a covered incident, your insurance policy will reimburse you for the cost of repairs or replacement of your damaged property, up to the policy limits.

- Home insurance can also cover additional expenses, such as temporary accommodation, if your home becomes uninhabitable due to damage.

- Having comprehensive home insurance can provide peace of mind knowing that you are financially protected in the event of an unexpected incident.

Closure

Finding the cheapest home insurance in Australia requires careful research and a proactive approach. By understanding the intricacies of policies, comparing quotes from reputable providers, and taking steps to mitigate risks, you can secure the best possible protection for your home while staying within your budget. Remember, home insurance is an essential investment that provides peace of mind and financial security in the event of unforeseen circumstances. Don’t settle for the first quote you receive; take the time to explore your options and find the policy that best suits your needs and circumstances.

FAQ Guide

What are the common types of home insurance available in Australia?

Common types of home insurance in Australia include building insurance, contents insurance, and combined building and contents insurance. Building insurance covers the structure of your home, while contents insurance protects your belongings. Combined policies offer coverage for both.

How often should I review my home insurance policy?

It’s recommended to review your home insurance policy annually or whenever there are significant changes to your property, belongings, or risk profile. This ensures your coverage remains adequate and reflects your current circumstances.

What are some tips for negotiating lower insurance premiums?

To negotiate lower premiums, consider increasing your deductible, bundling policies with the same provider, installing security features, and seeking discounts for loyalty, good driving records, or membership in certain organizations.