Table of contents:

Do beneficiaries pay tax on life insurance in Australia? This question is often on the minds of those considering life insurance, as well as their loved ones who may one day receive the proceeds. In Australia, the tax treatment of life insurance payouts can be complex, depending on various factors like the type of policy, the relationship between the beneficiary and the deceased, and the amount of the payout. Understanding these nuances is crucial for both policyholders and beneficiaries to ensure that the intended benefits are received without any unexpected tax liabilities.

This guide will delve into the intricacies of Australian life insurance taxation, providing a clear understanding of the rules and regulations that govern the taxability of life insurance proceeds. We’ll explore different types of life insurance policies, discuss the concept of “death benefit” and its tax implications, and examine the conditions under which life insurance payouts are considered tax-free or subject to taxation. Additionally, we’ll provide insights into reporting requirements, payment deadlines, and potential penalties for non-compliance.

Life Insurance Basics in Australia

Life insurance provides financial security for your loved ones in the event of your death. It pays a lump sum benefit to your designated beneficiaries, helping them cope with financial challenges and ensuring their well-being.

Types of Life Insurance Policies

Life insurance policies in Australia come in various forms, each catering to specific needs and financial situations.

- Term Life Insurance: This type provides coverage for a fixed period, typically 10 to 30 years. It’s generally the most affordable option and is ideal for covering short-term financial obligations, such as a mortgage or young children’s education.

- Permanent Life Insurance: This offers lifelong coverage, providing a death benefit regardless of when you pass away. It’s more expensive than term life insurance but offers additional features like investment options and cash value accumulation.

- Whole Life Insurance: A type of permanent life insurance, whole life insurance offers fixed premiums and guaranteed cash value growth. It’s suitable for long-term financial planning and legacy building.

- Universal Life Insurance: Another type of permanent life insurance, universal life insurance provides flexible premiums and cash value growth based on market performance. It offers greater control over your policy but requires more active management.

- Group Life Insurance: Offered through employers or organizations, group life insurance provides coverage to members at a lower cost than individual policies. It’s typically a term life insurance policy with a fixed benefit amount.

Beneficiary

A beneficiary is the person or entity designated to receive the death benefit from your life insurance policy. You can choose one or multiple beneficiaries and specify the percentage of the benefit each will receive.

Claiming Life Insurance Benefits

When you pass away, your beneficiaries need to file a claim with the life insurance company to receive the death benefit. The process typically involves providing documentation, such as a death certificate, policy details, and beneficiary information. The life insurance company will review the claim and, if approved, disburse the benefit to the designated beneficiaries.

Tax Implications of Life Insurance Proceeds

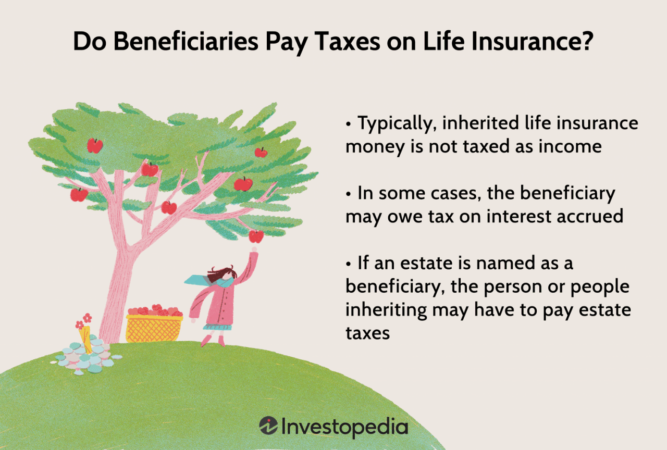

In Australia, life insurance payouts are generally tax-free for beneficiaries. This means that the money received from a life insurance policy is not subject to income tax. However, there are some specific circumstances where tax may apply.

Tax Treatment of Life Insurance Proceeds

The tax treatment of life insurance proceeds depends on the type of policy and the relationship between the beneficiary and the deceased. Generally, life insurance proceeds are considered a “death benefit” and are tax-free in the hands of the beneficiary. This means that the beneficiary does not have to pay any income tax on the money received.

Death Benefit

A “death benefit” is the payment made by a life insurance company to the beneficiary of a life insurance policy upon the death of the insured person. The death benefit is generally tax-free in the hands of the beneficiary, regardless of their relationship with the deceased. However, there are some exceptions to this rule.

Tax Implications for Beneficiaries

The tax implications for beneficiaries depend on their relationship with the deceased and the type of life insurance policy.

- Spouse or Dependant: If the beneficiary is the spouse or a dependant of the deceased, the death benefit is generally tax-free. This is because the death benefit is considered a “gift” from the deceased to the beneficiary.

- Other Beneficiaries: If the beneficiary is not the spouse or a dependant of the deceased, the death benefit may be subject to tax. This is because the death benefit is considered “income” to the beneficiary.

Tax-Free Life Insurance Proceeds

In Australia, life insurance payouts are generally tax-free for beneficiaries. This means that the beneficiary does not have to pay any income tax on the money they receive from the life insurance policy. However, there are certain conditions that must be met for the proceeds to be tax-free.

There are specific conditions under which life insurance payouts are tax-free for beneficiaries. These conditions are generally straightforward and aim to ensure the proceeds are truly intended for the beneficiary’s benefit and not for other purposes.

Superannuation Death Benefit

Superannuation death benefits are payments made from a superannuation fund to a beneficiary upon the death of a member. These benefits are generally tax-free for the beneficiary. This tax-free status applies regardless of the beneficiary’s relationship to the deceased member, whether it’s a spouse, partner, child, or other dependent.

Exemptions and Exceptions

While life insurance payouts are generally tax-free, there are some exceptions to this rule. For example, if the proceeds are paid to a beneficiary who is not a dependent of the deceased, the beneficiary may be required to pay tax on the proceeds. This is because the proceeds may be considered a taxable income for the beneficiary in this scenario.

Another exception is if the life insurance policy was taken out for business purposes. In this case, the proceeds may be subject to tax. This is because the proceeds may be considered a taxable income for the business.

Taxable Life Insurance Proceeds

While life insurance proceeds are generally tax-free in Australia, there are specific situations where they become taxable. This typically occurs when the insurance policy is structured in a way that generates a financial gain beyond the pure death benefit.

Taxable Life Insurance Proceeds Examples

Taxable life insurance proceeds often arise when the policyholder receives a payout exceeding the death benefit or when the policy is used for investment purposes. Here are some examples:

- Surrenders and Maturities: If you surrender a life insurance policy before its maturity date or when it reaches its maturity, any gains exceeding the original premiums paid are considered taxable income. This applies to both traditional life insurance and investment-linked policies.

- Investment-Linked Policies: These policies, also known as “with-profits” policies, invest a portion of the premiums in the market. If the investment component generates substantial gains, the portion exceeding the original premiums paid is taxable income.

- Endowment Policies: These policies combine a life insurance component with a savings component. The savings component typically matures after a certain period, and any gains exceeding the premiums paid are considered taxable income.

Tax Calculation Methods

The tax liability on taxable life insurance proceeds is calculated based on the nature of the income and the individual’s tax bracket.

- Ordinary Income: Gains from surrendering a policy, maturing a policy, or from investment-linked policies are generally considered ordinary income. This income is taxed at the individual’s marginal tax rate.

- Capital Gains: If the policy is held for more than 12 months, the gains are considered capital gains. Capital gains are taxed at a lower rate than ordinary income, and there is a discount available for long-term capital gains.

The tax calculation for taxable life insurance proceeds is complex and depends on various factors, including the policy type, the period of holding, and the individual’s tax situation. It’s recommended to seek professional advice from a qualified financial advisor or tax accountant to determine the specific tax implications for your circumstances.

Reporting and Payment of Taxes

You’ll need to report any taxable life insurance payouts to the Australian Taxation Office (ATO). This ensures you’re paying the correct amount of tax on your income, including any proceeds from life insurance policies.

Reporting Taxable Life Insurance Proceeds

The ATO requires you to report taxable life insurance proceeds on your tax return. You’ll need to provide details about the policy, the amount received, and any deductions you’re claiming. You can do this by using the relevant section in your tax return form or by using the ATO’s online services.

Deadlines for Filing Tax Returns

The deadline for filing your tax return depends on your circumstances. If you’re an individual, the deadline is usually October 31st of the following financial year. However, if you have a tax agent, they may have a different deadline. It’s important to check the ATO’s website for the most up-to-date information.

Penalties for Non-Compliance, Do beneficiaries pay tax on life insurance in australia

Failing to report or pay taxes on life insurance proceeds can result in penalties. The ATO can impose penalties for late lodgement, incorrect information, or failure to pay tax. These penalties can be significant, so it’s essential to comply with your tax obligations.

Seeking Professional Advice

While this guide provides a comprehensive overview of life insurance taxation in Australia, it’s essential to remember that every situation is unique. Seeking professional advice from a qualified financial advisor or tax specialist is crucial for personalized guidance tailored to your specific circumstances.

Types of Professional Advice

The type of professional advice you need will depend on your individual situation and the complexity of your life insurance arrangements. Here are some examples of the types of advice you may need:

- Financial Advisor: A financial advisor can help you understand your overall financial goals and develop a strategy that includes life insurance. They can help you determine the appropriate amount of life insurance coverage and recommend suitable policies based on your needs and risk tolerance.

- Tax Specialist: A tax specialist can provide expert advice on the tax implications of your life insurance policy. They can help you understand the rules surrounding tax-free and taxable life insurance proceeds and ensure you comply with all reporting requirements.

- Insurance Broker: An insurance broker can help you compare different life insurance policies from various providers. They can assist you in finding the best policy that meets your specific needs and budget.

Benefits of Seeking Professional Guidance

Seeking professional guidance from a qualified advisor can offer several benefits, including:

- Personalized Advice: An advisor can provide tailored recommendations based on your unique circumstances, ensuring your life insurance strategy aligns with your financial goals and tax situation.

- Minimizing Tax Liability: A tax specialist can help you structure your life insurance arrangements to minimize your tax obligations. They can advise on strategies for maximizing tax-free benefits and minimizing taxable income.

- Peace of Mind: Having a professional guide you through the complexities of life insurance and taxation can provide peace of mind, knowing that your financial interests are well-protected.

- Avoiding Errors: A professional advisor can help you avoid costly mistakes by ensuring you comply with all relevant tax laws and regulations.

Epilogue

Navigating the complexities of life insurance taxation in Australia can be daunting. While the general rule is that life insurance payouts are tax-free for beneficiaries, there are specific exceptions and nuances that require careful consideration. Consulting a financial advisor or tax specialist is highly recommended to ensure that you fully understand the tax implications of your life insurance policy and receive personalized guidance tailored to your individual circumstances. By seeking professional advice, you can gain peace of mind knowing that your loved ones will receive the intended benefits of your life insurance policy without any unexpected tax burdens.

FAQ Resource: Do Beneficiaries Pay Tax On Life Insurance In Australia

What types of life insurance policies are available in Australia?

Australia offers various life insurance policies, including term life insurance, whole life insurance, and endowment policies. Each policy type has its own features, benefits, and premiums.

What is a “death benefit” in life insurance?

A “death benefit” is the lump sum payment made to the beneficiary upon the death of the insured person. This benefit is typically paid out from the life insurance policy.

Can I claim life insurance benefits if I’m not the named beneficiary?

Generally, only the named beneficiary can claim life insurance benefits. However, there may be exceptions depending on the policy terms and the specific circumstances.

How do I report taxable life insurance payouts to the ATO?

Taxable life insurance payouts should be reported on your annual tax return using the relevant forms and schedules provided by the ATO.