Table of contents:

How much does car insurance cost in Australia? This question is on the minds of many Australians, as the cost of car insurance can vary significantly depending on a range of factors. From your age and driving history to the type of vehicle you drive, numerous elements influence your premiums. Understanding these factors can help you make informed decisions about your car insurance and potentially save money.

This guide explores the key factors that affect car insurance costs in Australia, providing a comprehensive overview of the different types of coverage available, how to obtain quotes, and essential tips for saving money.

Factors Influencing Car Insurance Costs: How Much Does Car Insurance Cost In Australia

Car insurance premiums in Australia are influenced by a variety of factors, including your personal details, your driving history, and the vehicle you own. These factors are used by insurance companies to assess your risk and determine how much you will pay for coverage.

Age

Your age is a significant factor in determining your car insurance premium. Younger drivers are generally considered to be at higher risk of accidents, due to their lack of experience and potentially more risky driving habits. As you age, you gain more driving experience, which reduces your risk profile and consequently, your insurance premiums.

Driving History

Your driving history plays a crucial role in determining your insurance costs. A clean driving record with no accidents or traffic violations will result in lower premiums. Conversely, a history of accidents, speeding tickets, or other offenses will increase your premiums. This is because your driving history reflects your driving habits and your potential risk of future accidents.

Location

The location where you live can also influence your car insurance costs. Areas with higher crime rates, traffic congestion, and more accidents tend to have higher insurance premiums. This is because insurance companies consider these factors to be riskier for drivers.

Vehicle Type, Make, and Model

The type, make, and model of your vehicle significantly impact your insurance premiums. Vehicles that are considered more expensive to repair, more prone to theft, or have a higher risk of accidents will generally have higher insurance premiums. For example, a high-performance sports car will typically cost more to insure than a standard family sedan.

Driving Experience

Your driving experience is another key factor influencing your insurance costs. The more experience you have behind the wheel, the less likely you are to be involved in an accident. Insurance companies often offer discounts to drivers with several years of driving experience.

Claims History

Your claims history is a significant factor in determining your insurance premiums. If you have made a claim in the past, it indicates a higher risk of future claims. This will likely result in higher premiums. Conversely, if you have a clean claims history, you will likely qualify for lower premiums.

No-Claims Bonus

A no-claims bonus is a discount offered by insurance companies to drivers who have not made any claims for a certain period. The longer you go without making a claim, the higher your no-claims bonus will be. This is a significant way to reduce your insurance premiums over time.

Types of Car Insurance Coverage

In Australia, there are several types of car insurance available, each offering different levels of protection and financial coverage. Understanding the distinctions between these options is crucial for making an informed decision that aligns with your individual needs and risk tolerance.

Comprehensive Car Insurance, How much does car insurance cost in australia

Comprehensive car insurance provides the most comprehensive coverage, protecting you against a wide range of risks, including:

* Accidents: Covers damage to your vehicle, regardless of who is at fault, in case of an accident.

* Theft: Reimburses you for the loss of your vehicle if it is stolen.

* Fire: Protects against damage caused by fire.

* Natural Disasters: Covers damage caused by events like floods, earthquakes, and hailstorms.

* Vandalism: Provides coverage for damage resulting from vandalism or malicious acts.

- Benefits: Comprehensive insurance offers the highest level of protection, providing peace of mind knowing that you are covered against a wide range of risks. This can be particularly beneficial if you drive an expensive car or live in an area prone to theft or natural disasters.

- Drawbacks: Comprehensive insurance is typically the most expensive type of car insurance. However, the higher premium reflects the extensive coverage it provides.

Third-Party Property Damage Insurance

This type of insurance covers damage you cause to another person’s vehicle or property in an accident, but does not cover damage to your own vehicle.

- Benefits: Third-party property damage insurance is generally more affordable than comprehensive insurance. It offers basic protection against liability claims, ensuring you are covered if you are at fault in an accident.

- Drawbacks: This type of insurance does not cover damage to your own vehicle. If you are involved in an accident where your car is damaged, you will be responsible for the repair costs.

Third-Party Fire and Theft Insurance

This type of insurance provides coverage for your vehicle against fire and theft, but not for damage caused by accidents.

- Benefits: Third-party fire and theft insurance offers a middle ground between comprehensive and third-party property damage insurance. It is more affordable than comprehensive insurance while providing protection against specific risks like fire and theft.

- Drawbacks: It does not cover damage to your vehicle in an accident. This means you will be responsible for repair costs if your vehicle is damaged in a collision.

Cost Comparison of Different Coverage Types

The cost of car insurance varies depending on factors such as your age, driving history, vehicle type, and location. However, a general comparison of the costs of different coverage types is shown below:

| Coverage Type | Hypothetical Premium (Annual) |

|---|---|

| Comprehensive | $1,500 |

| Third-Party Property Damage | $800 |

| Third-Party Fire and Theft | $1,000 |

Note: These are hypothetical examples and actual premiums may vary significantly based on individual circumstances.

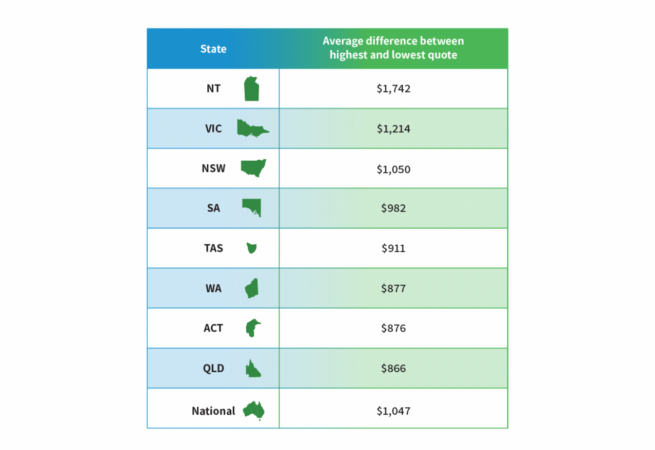

Obtaining Car Insurance Quotes

Getting car insurance quotes is a crucial step in securing the right coverage for your vehicle. It allows you to compare prices, coverage options, and insurer features to find the best value for your needs.

Comparing Quotes from Multiple Insurers

It is essential to compare quotes from multiple insurers before making a decision. This ensures you get the best possible price and coverage for your specific needs.

- Comparing quotes helps you identify the most competitive rates and coverage options available.

- By comparing quotes, you can save money on your car insurance premiums.

- It also allows you to find an insurer that meets your specific needs, such as a company with a strong reputation for customer service or a specific type of coverage.

Factors to Consider When Choosing an Insurer

When choosing an insurer, it is important to consider various factors beyond just price. These factors include:

- Price: Price is often the primary factor in choosing an insurer. However, it is essential to consider the coverage you are getting for the price. A cheaper policy may not offer the same level of protection as a more expensive policy.

- Coverage: Coverage refers to the types of risks your policy protects you against. Consider your individual needs and the risks you face, such as accidents, theft, or natural disasters, when evaluating coverage options.

- Customer Service: A good insurer will provide excellent customer service. This includes prompt and helpful responses to your inquiries, efficient claims processing, and a commitment to resolving issues fairly and quickly. Look for insurers with a good reputation for customer service.

- Financial Stability: Choosing a financially stable insurer is crucial, as it ensures they can pay claims in the event of an accident or other covered event. You can research an insurer’s financial strength by checking their ratings with independent agencies like AM Best or Standard & Poor’s.

Understanding Car Insurance Policies

It’s essential to thoroughly understand your car insurance policy to ensure you’re adequately covered and aware of your rights and obligations. This section delves into key terms, conditions, claim processes, and common exclusions found in car insurance policies.

Key Terms and Conditions

Car insurance policies contain specific terms and conditions that define the coverage you’re entitled to. Here are some of the most common:

- Excess: This is the amount you’ll have to pay towards any claim, regardless of the coverage level. It’s typically a fixed amount, but can vary depending on the policy and the type of claim.

- Premium: This is the amount you pay for your insurance coverage, usually paid monthly or annually. It’s calculated based on various factors like your driving history, vehicle details, and the level of coverage you choose.

- Sum insured: This refers to the maximum amount the insurer will pay out for a claim. It’s important to ensure the sum insured is adequate to cover the value of your vehicle and potential repair costs.

- Policy period: This is the duration for which your insurance coverage is valid, typically for a year. It’s crucial to renew your policy before it expires to maintain continuous coverage.

- No-claim bonus (NCB): This is a discount offered by insurers for not making any claims during a specific period. The NCB increases with each claim-free year, offering significant savings on premiums.

Making a Claim

When you need to make a claim, you’ll need to contact your insurer and provide them with all the necessary details. Here’s a general overview of the process:

- Report the incident: Contact your insurer immediately after the accident or incident, providing them with details about the event, including the date, time, location, and any injuries involved.

- Gather documentation: You’ll need to provide your insurer with relevant documentation, including a police report if applicable, photos of the damage, and any witness statements. If you’re claiming for injuries, you may need medical reports and invoices for treatment costs.

- Assessment and approval: Your insurer will assess the claim and determine if it’s covered under your policy. They may need to inspect the damage to your vehicle and investigate the circumstances of the incident.

- Claim settlement: Once your claim is approved, your insurer will pay out the agreed-upon amount. This could involve repairing your vehicle, covering medical expenses, or paying out a lump sum for the total loss of your vehicle.

Common Exclusions and Limitations

It’s essential to be aware of the exclusions and limitations in your policy. These are situations where your insurance coverage may not apply. Some common exclusions include:

- Driving under the influence of alcohol or drugs: Insurers generally won’t cover claims if the driver was intoxicated or under the influence of drugs at the time of the accident.

- Driving without a valid license: If you’re driving without a valid driver’s license, your insurance coverage may be void.

- Using the vehicle for illegal activities: Claims related to illegal activities, such as transporting stolen goods or engaging in criminal acts, are unlikely to be covered.

- Wear and tear: General wear and tear on your vehicle is not usually covered by insurance. For example, a flat tire due to normal wear and tear is not typically covered.

- Acts of God: While some policies may offer limited coverage for events like earthquakes or floods, they’re often excluded or subject to specific limitations.

Tips for Saving on Car Insurance

In Australia, car insurance can be a significant expense, but there are ways to lower your premiums and save money. By implementing some simple strategies and making informed decisions, you can reduce your insurance costs and keep more money in your pocket.

Safe Driving Practices

Adopting safe driving practices can significantly impact your insurance premiums. Insurance companies reward safe drivers with lower rates. Here are some tips to reduce your risk and potentially save money:

- Maintain a Clean Driving Record: A clean driving record with no accidents, speeding tickets, or other traffic violations is crucial for securing lower premiums. Insurance companies consider your driving history a key factor in determining your risk profile.

- Defensive Driving Courses: Enrolling in a defensive driving course can demonstrate your commitment to safe driving and potentially earn you discounts. These courses teach valuable techniques for avoiding accidents and navigating challenging driving situations.

- Avoid Distracted Driving: Distracted driving is a major cause of accidents. Avoid using your phone, eating, or engaging in other distractions while driving. Focus on the road and practice safe driving habits.

Vehicle Modifications

Modifying your vehicle can affect your insurance premiums. Some modifications might increase your risk, while others can lower it.

- Anti-theft Devices: Installing anti-theft devices, such as alarms, immobilizers, or tracking systems, can make your vehicle less attractive to thieves. This can lower your insurance premiums as it reduces the risk of theft.

- Safety Features: Vehicles equipped with advanced safety features, such as anti-lock brakes, electronic stability control, or airbags, generally have lower insurance premiums. These features can enhance your safety and reduce the likelihood of accidents.

Bundling Insurance Policies

Bundling your car insurance with other insurance policies, such as home, contents, or health insurance, can lead to significant savings. Insurance companies often offer discounts for customers who bundle multiple policies with them.

Seeking Discounts

Many insurance companies offer discounts to various groups or for specific circumstances. Some common discounts include:

- Good Student Discount: Students with good academic records may qualify for a discount. This demonstrates responsible behavior and lower risk.

- Safe Driver Discount: Drivers with a clean driving record and no accidents or violations can qualify for a safe driver discount. This reflects their lower risk profile.

- Loyalty Discount: Long-term customers with a good history with the insurance company may be eligible for a loyalty discount. This rewards customer loyalty and retention.

- Multi-car Discount: If you insure multiple vehicles with the same company, you may qualify for a multi-car discount. This reflects the reduced risk associated with insuring multiple vehicles.

Negotiating Lower Insurance Rates

Negotiating lower insurance rates with providers can be a worthwhile endeavor. Here are some tips to leverage your bargaining power:

- Shop Around: Obtain quotes from multiple insurance companies to compare rates and coverage options. This allows you to find the best value for your needs.

- Review Your Policy: Carefully review your existing policy and identify any unnecessary coverage or exclusions. You can negotiate to remove or adjust these aspects to lower your premium.

- Consider Your Driving Habits: If you drive less frequently or only for short distances, you might qualify for a lower premium based on your driving habits. Discuss this with your insurer.

- Be Prepared to Switch: Having multiple quotes from different companies gives you leverage to negotiate a lower rate with your current provider. If they are unwilling to match or beat a competitor’s offer, you can switch to a more affordable insurer.

End of Discussion

Navigating the world of car insurance in Australia can seem complex, but with a clear understanding of the factors that influence costs and the different coverage options available, you can make informed decisions to ensure you’re getting the best value for your money. By comparing quotes from multiple insurers, considering your individual needs, and implementing smart strategies to reduce premiums, you can find a car insurance policy that provides the right level of protection at a price that fits your budget.

Key Questions Answered

What are the main types of car insurance in Australia?

The most common types of car insurance in Australia are comprehensive, third-party property damage, and third-party fire and theft. Comprehensive coverage offers the broadest protection, while third-party property damage and third-party fire and theft provide more limited coverage.

How can I find the cheapest car insurance in Australia?

The best way to find cheap car insurance is to compare quotes from multiple insurers. Use online comparison websites or contact insurers directly to get personalized quotes.

What are some common discounts offered by car insurance companies in Australia?

Common discounts include no-claims bonuses, safe driver discounts, multi-policy discounts (bundling home and car insurance), and discounts for certain vehicle features like anti-theft devices.