Table of contents:

What is a yearly deductible for health insurance? It’s a crucial concept in understanding the costs associated with healthcare coverage. Simply put, a deductible is the amount you must pay out-of-pocket for medical expenses before your health insurance starts covering the rest. Think of it as a threshold you need to reach before your insurance kicks in.

Imagine you have a $1,000 yearly deductible on your health insurance plan. If you incur $500 in medical expenses, you’ll pay the entire $500 yourself. However, if your medical expenses reach $1,500, you’ll pay the first $1,000 (your deductible) and your insurance will cover the remaining $500.

What is a Deductible?: What Is A Yearly Deductible For Health Insurance

A deductible is a fixed amount of money that you, as the policyholder, are required to pay out-of-pocket before your health insurance plan starts covering your medical expenses. It’s like a threshold you need to cross before your insurance kicks in.

How Deductibles Work

Imagine you have a health insurance plan with a $1,000 deductible. If you incur $500 in medical expenses, you’ll be responsible for paying the entire $500 yourself. However, if your medical expenses reach $1,500, you’ll pay the first $1,000 (your deductible) and your insurance will cover the remaining $500.

When You Might Have to Pay Your Deductible

You’ll typically have to pay your deductible for:

- Inpatient hospital stays: If you need to be admitted to the hospital, you might have to pay your deductible before your insurance starts covering your hospital bills.

- Outpatient services: This includes doctor’s visits, lab tests, and other medical services that don’t require an overnight hospital stay.

- Prescription drugs: Some health insurance plans have separate deductibles for prescription drugs. You’ll need to meet this deductible before your insurance starts covering your prescription costs.

Yearly Deductible vs. Other Deductibles

A yearly deductible is a common type of deductible, but it’s not the only one. Understanding how different types of deductibles work is essential for making informed decisions about your health insurance plan.

Yearly Deductible vs. Per-Incident Deductible, What is a yearly deductible for health insurance

Yearly deductibles are typically applied to all covered medical expenses within a calendar year. In contrast, per-incident deductibles are applied separately to each medical event or incident.

Here’s a breakdown of the differences:

- Yearly Deductible: You pay a set amount toward your healthcare costs for the entire year, regardless of the number of medical events. Once you reach your yearly deductible, your insurance plan starts covering a larger percentage of your medical expenses.

- Per-Incident Deductible: You pay a set amount for each medical event, such as a hospital stay, surgery, or doctor’s visit. Once you reach the per-incident deductible, your insurance plan starts covering the remaining costs for that particular incident.

For example, imagine you have a health insurance plan with a $2,000 yearly deductible and a $500 per-incident deductible.

- Yearly Deductible: If you have a medical bill of $1,000 in January and another of $1,500 in June, you would pay the full $1,000 for the first bill. For the second bill, you would pay the remaining $500 to reach your yearly deductible, and your insurance would then cover the rest.

- Per-Incident Deductible: If you have a $1,000 medical bill in January and a $1,500 medical bill in June, you would pay $500 for each bill, as this is less than the per-incident deductible.

Benefits and Drawbacks

Each type of deductible offers advantages and disadvantages:

- Yearly Deductible:

- Benefits: You may pay less overall if you have multiple medical events in a year, as you only need to meet the deductible once.

- Drawbacks: You may face a higher upfront cost if you have a major medical event early in the year.

- Per-Incident Deductible:

- Benefits: You may have lower out-of-pocket costs for each individual medical event.

- Drawbacks: You could end up paying more overall if you have multiple medical events in a year, as you’ll need to meet the deductible for each incident.

Ultimately, the best type of deductible for you depends on your individual needs and health history. Consider your expected healthcare costs, how often you typically visit the doctor, and your risk tolerance.

Factors Influencing Deductible Amount

Your yearly deductible amount is influenced by several factors, including your age, health status, and the type of health insurance plan you choose. Understanding these factors can help you select a plan that aligns with your needs and budget.

Age

Your age is a significant factor that insurance companies consider when setting your deductible. Younger individuals generally have lower deductibles compared to older individuals. This is because younger individuals tend to be healthier and require fewer medical services.

Health Status

Your health status also plays a role in determining your deductible. Individuals with pre-existing health conditions may have higher deductibles than those who are generally healthy. This is because insurance companies anticipate higher healthcare costs for individuals with pre-existing conditions.

Plan Type

The type of health insurance plan you choose significantly influences your deductible. Here is a table comparing deductible amounts for different health insurance plans:

| Plan Type | Deductible Range |

|---|---|

| High Deductible Health Plan (HDHP) | $1,400 – $7,000 (individual) $2,800 – $14,000 (family) |

| Preferred Provider Organization (PPO) | $500 – $2,500 (individual) $1,000 – $5,000 (family) |

| Health Maintenance Organization (HMO) | $0 – $1,000 (individual) $0 – $2,000 (family) |

Calculating Total Cost of Health Insurance

To calculate the total cost of your health insurance, you need to consider several factors beyond the deductible:

Total Cost = Monthly Premium + Out-of-Pocket Costs + Deductible

For example, if your monthly premium is $300, your deductible is $1,000, and you have $500 in out-of-pocket costs, your total cost for the year would be:

$300 x 12 + $1,000 + $500 = $4,600

The Role of Deductibles in Cost Sharing

Deductibles play a crucial role in the concept of cost sharing in health insurance. Cost sharing is a mechanism where both the insurance company and the insured individual share the financial burden of healthcare expenses. It encourages individuals to be more mindful of their healthcare utilization, as they are directly involved in the cost of their medical care.

Cost Sharing After Meeting the Deductible

Once the deductible is met, cost sharing continues to apply to subsequent medical expenses. This means that you will still be responsible for a portion of the costs, even though you have already paid the deductible. This cost sharing is typically implemented through coinsurance and copayments.

Coinsurance is a percentage of the medical expenses that you are responsible for paying after the deductible has been met.

Copayments are fixed amounts that you pay for specific services, such as doctor’s visits or prescriptions.

For example, imagine a person with a $2,000 deductible and a 20% coinsurance rate. If they incur $5,000 in medical expenses, they would first pay the $2,000 deductible. Then, they would be responsible for 20% of the remaining $3,000, which is $600. The insurance company would cover the remaining $2,400.

Typical Cost Sharing Percentages for Different Medical Services

The following table Artikels typical cost sharing percentages for different types of medical services:

| Medical Service | Coinsurance Percentage | Copayment Amount |

|---|---|---|

| Doctor’s Visits | 20% | $20-$50 |

| Hospital Stays | 20% | N/A |

| Prescription Drugs | 20% | $10-$40 |

| Mental Health Services | 20% | $20-$50 |

It’s important to note that these are just typical percentages and can vary significantly depending on the specific health insurance plan. It is essential to review your plan documents to understand the exact cost sharing percentages and copayments that apply to your coverage.

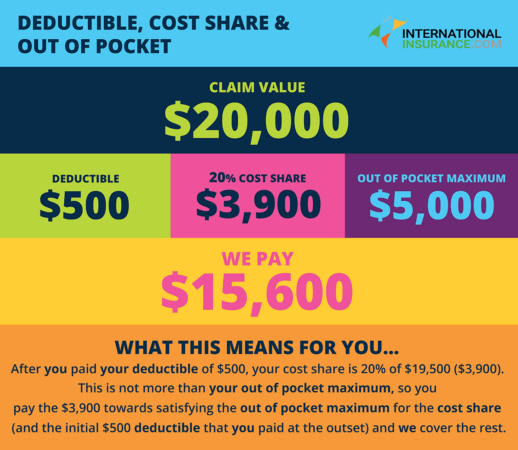

Deductible and Out-of-Pocket Maximum

Both the deductible and the out-of-pocket maximum are important concepts in health insurance. While they seem similar, they play distinct roles in how you pay for your healthcare. Understanding their differences and relationship is crucial to making informed decisions about your health insurance coverage.

The Relationship Between Deductible and Out-of-Pocket Maximum

The deductible and the out-of-pocket maximum work together to limit your financial responsibility for healthcare costs in a given year. The deductible is the amount you must pay out-of-pocket before your insurance starts covering your medical expenses. Once you meet your deductible, your insurance company starts paying a larger portion of your healthcare costs. The out-of-pocket maximum is the total amount you’ll have to pay for covered healthcare expenses in a year, including your deductible, coinsurance, and copayments. After reaching this limit, your insurance will cover 100% of your covered medical expenses for the rest of the year.

Example Scenario

Imagine you have a health insurance plan with a $2,000 deductible and a $5,000 out-of-pocket maximum. You need to undergo a surgery that costs $10,000.

- First, you’ll need to pay the $2,000 deductible out-of-pocket.

- After paying the deductible, your insurance will start covering the remaining costs. If your coinsurance is 20%, you’ll pay 20% of the remaining $8,000, which is $1,600.

- In this scenario, your total out-of-pocket expenses would be $3,600 ($2,000 deductible + $1,600 coinsurance).

- Since you’ve reached your out-of-pocket maximum of $5,000, your insurance will cover 100% of any further medical expenses for the rest of the year.

Conclusive Thoughts

Understanding your yearly deductible is essential for making informed decisions about your health insurance plan. By knowing how deductibles work and the factors that influence their amount, you can choose a plan that aligns with your healthcare needs and budget. Remember, deductibles are just one piece of the cost-sharing puzzle in health insurance, and they play a significant role in determining your overall healthcare expenses.

Frequently Asked Questions

How does a deductible affect my co-pays and coinsurance?

Once you meet your deductible, your co-pays and coinsurance apply to the remaining covered medical expenses. These are fixed amounts or percentages you pay for services, typically after your deductible is met.

What happens if I change health insurance plans mid-year?

If you switch plans mid-year, you usually start a new deductible period. However, some plans may offer credit for deductibles already paid towards your previous plan. Check with your insurance provider for specific details.

Can I pay my deductible in installments?

This depends on your insurance provider. Some insurers allow you to pay your deductible in installments, while others require a lump sum payment. It’s best to inquire about your plan’s specific payment options.